If you earn £125,000 a year, your monthly take-home pay in the UK in 2026 is roughly £6,504.84 after Income Tax and employee National Insurance, assuming you are on a standard tax code, have no pension salary sacrifice, and do not live in Scotland.

This means:

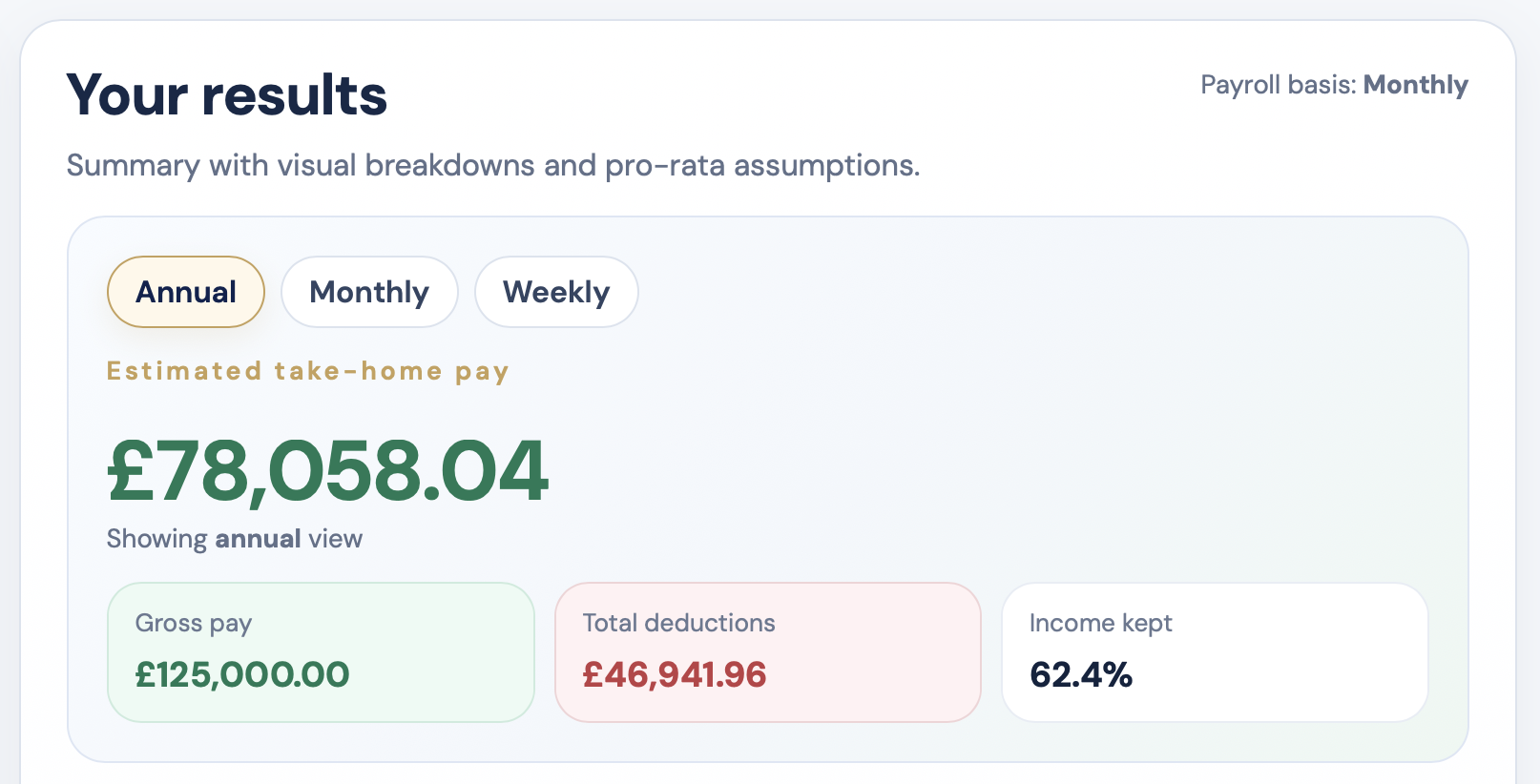

- Annual take-home pay: £78,058.04

- Monthly take-home pay: £6,504.84

- Weekly take-home pay: ~£1,501

This guide explains exactly how your £125,000 salary is taxed, how much you take home each month, and what factors can change your net pay.

This calculation is based on the 2026/27 UK tax year using the figures provided here.

If you want to test your own payslip with pension, bonus or student loan deductions, use our take home pay calculator for a personalised result.

£125,000 take-home pay UK (2026 summary)

- Gross salary: £125,000

- 20% Income Tax: £7,539.96

- 40% Income Tax: £34,892.04

- National Insurance: £4,509.96

- Net annual pay: £78,058.04

- Net monthly pay: £6,504.84

- Net weekly pay: ~£1,501

£125,000 salary after tax in the UK: monthly and annual breakdown

| Item | Annual | Monthly |

|---|---|---|

| Gross salary | £125,000.00 | £10,416.67 |

| 20% Income Tax | £7,539.96 | £628.33 |

| 40% Income Tax | £34,892.04 | £2,907.67 |

| Employee National Insurance | £4,509.96 | £375.83 |

| Take-home pay | £78,058.04 | £6,504.84 |

So for most employees in England, Wales and Northern Ireland, £125k after tax is about £6.5k per month.

£125,000 weekly take-home pay UK

If you earn £125,000 per year, your weekly take-home pay is approximately £1,501 after tax and National Insurance.

This is useful for:

- High-level budgeting and financial planning

- Comparing senior roles or contract opportunities

- Understanding real disposable income after heavy taxation

How the tax is worked out

For the 2026 to 2027 tax year, the standard Personal Allowance is £12,570, but at £125,000 it is effectively fully removed due to the Personal Allowance taper.

On a £125,000 salary:

- Your Personal Allowance is reduced to near £0

- A portion is taxed at 20% = £7,539.96

- A large portion is taxed at 40% = £34,892.04

- Employee National Insurance totals about £4,509.96

At this level, you are fully exposed to higher-rate tax and have lost the benefit of the tax-free Personal Allowance entirely.

What is £125k per month before and after tax?

Before deductions, a £125,000 salary is £10,416.67 per month.

After Income Tax and National Insurance, that falls to around £6,504.84 per month.

- Gross monthly pay: £10,416.67

- Total monthly tax and NI: £3,911.83

- Net monthly pay: £6,504.84

The key consideration at £125,000: zero Personal Allowance

By the time you reach £125,000, your Personal Allowance has been fully removed due to the taper between £100,000 and £125,140.

This means:

- You no longer receive the £12,570 tax-free allowance

- Your entire income is effectively taxable

- You have already passed through the highly inefficient £100k–£125k range

This range is often described as having an effective 60% tax rate, because you are paying 40% tax while also losing your Personal Allowance.

At £125,000, that process is complete — but it means a significant portion of your income has been taxed very heavily on the way up.

How to manage tax at £125,000

At this salary, tax planning becomes essential rather than optional. The goal is to manage how much income is exposed to higher-rate tax and whether you can regain some Personal Allowance efficiency.

Common strategies people consider include:

- Increasing pension contributions

- Using salary sacrifice where available

- Managing bonus payments carefully

- Reducing adjusted net income below £125k or even £100k where possible

- Reviewing total deductions including student loans

Even small adjustments in taxable income can have a large effect in this range, especially if they move you back into a more efficient tax band.

Can a SIPP help if you earn £125,000?

Yes, a SIPP (Self-Invested Personal Pension) can be particularly powerful at this salary level.

At £125,000, a SIPP may help you:

- Reduce adjusted net income and potentially restore some Personal Allowance

- Avoid or reduce exposure to the effective 60% tax band

- Claim higher-rate tax relief on contributions

- Build long-term wealth in a tax-efficient structure

Many SIPPs use relief at source, where basic-rate tax relief is added automatically. Higher-rate taxpayers typically need to claim additional relief through HMRC.

If your employer offers salary sacrifice, that can sometimes be even more efficient than a SIPP because it may reduce both Income Tax and National Insurance. However, a SIPP still provides flexibility and additional contribution options.

If you want to model how pension contributions could affect your monthly net pay, use our take home pay calculator.

£125k salary after tax with student loan deductions

If you still repay a student loan, your real monthly take-home will be lower.

| Scenario | Annual take-home | Monthly take-home |

|---|---|---|

| No student loan | £78,058.04 | £6,504.84 |

| Plan 1 | £69,229.04 | £5,769.09 |

| Plan 2 | £69,452.72 | £5,787.73 |

| Plan 5 | £69,058.04 | £5,754.84 |

| Postgraduate Loan only | £71,818.04 | £5,984.84 |

The matching student loan deductions are:

- Plan 1: £8,829.00 per year or £735.75 per month

- Plan 2: £8,605.32 per year or £717.11 per month

- Plan 5: £9,000.00 per year or £750.00 per month

- Postgraduate Loan only: £6,240.00 per year or £520.00 per month

At this salary, a Plan 2 borrower loses roughly £717.11 per month, while a Plan 5 borrower loses about £750.00 per month.

You can estimate your repayments using our student loan calculator.

£125,000 vs £100,000 salary UK

Moving from £100,000 to £125,000 significantly increases your gross pay, but much of that increase is taxed very heavily due to the loss of Personal Allowance and higher-rate tax.

You can compare salary levels using our salary comparison calculator.

Monthly budgeting on a £125,000 salary

With a take-home of around £5,755 to £6,505 per month, many people can usually cover:

- Mortgage or rent payments

- Bills and utilities

- Transport and commuting

- Investments and pension contributions

- Lifestyle and discretionary spending

However, tax efficiency plays a much larger role at this level than at lower salaries.

Summary

A £125,000 salary after tax in the UK works out to about £78,058.04 per year or £6,504.84 per month in 2026 using the figures provided here.

Your real take-home may be closer to £5,755 to £5,985 per month if student loan deductions apply. At this level, planning around higher-rate tax, pension contributions, salary sacrifice, SIPPs and the loss of Personal Allowance becomes essential for maximising your net income.