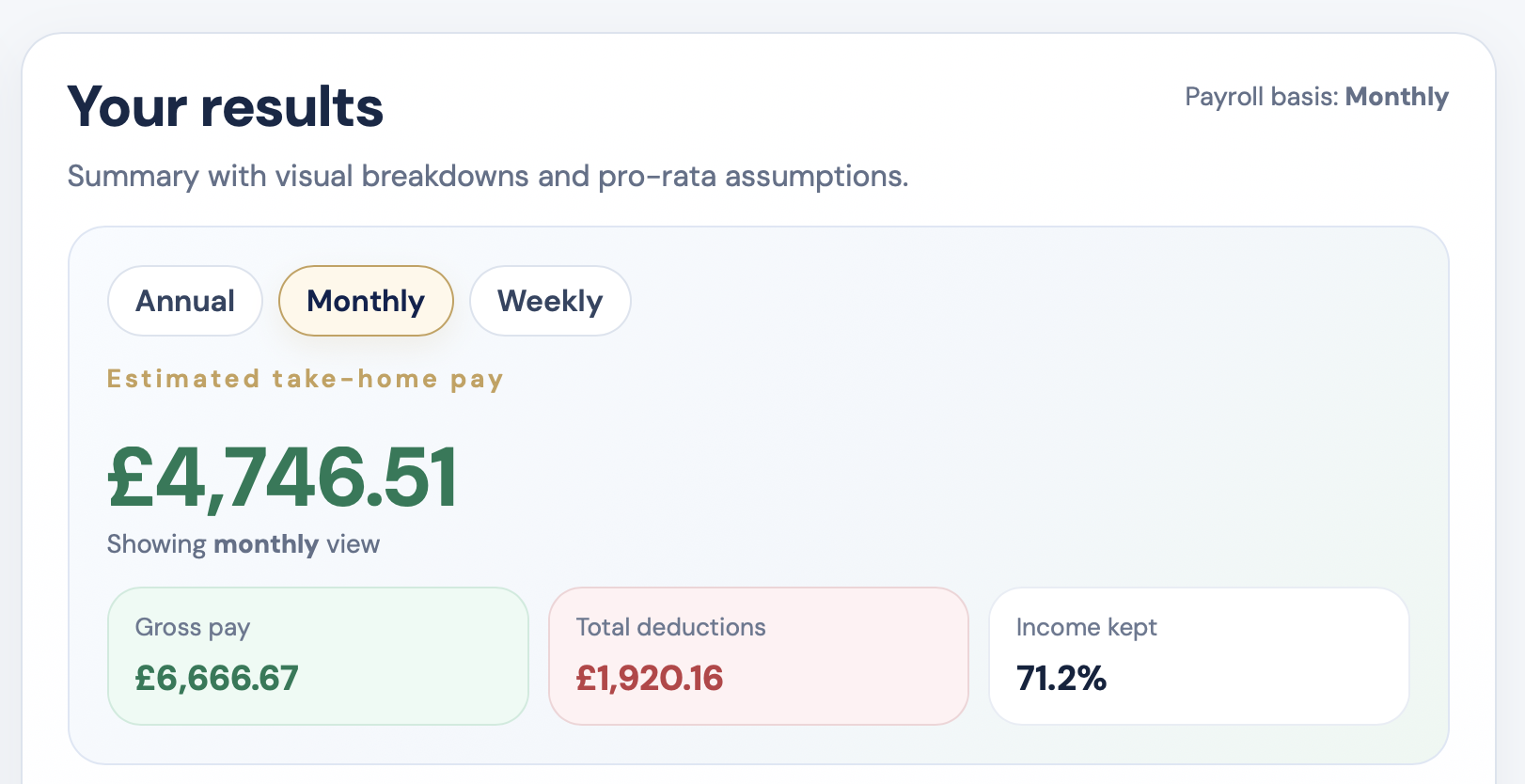

If you earn £80,000 a year, your monthly take-home pay in the UK in 2026 is roughly £4,746.51 after Income Tax and employee National Insurance, assuming you are on a standard tax code, have no pension salary sacrifice, and do not live in Scotland.

This means:

- Annual take-home pay: £56,958.08

- Monthly take-home pay: £4,746.51

- Weekly take-home pay: ~£1,095

This guide explains exactly how your £80,000 salary is taxed, how much you take home each month, and what factors can change your net pay.

This calculation is based on the 2026/27 UK tax year using the figures provided here.

If you want to test your own payslip with pension, bonus or student loan deductions, use our take home pay calculator for a personalised result.

£80,000 take-home pay UK (2026 summary)

- Gross salary: £80,000

- 20% Income Tax: £7,539.96

- 40% Income Tax: £11,892.00

- National Insurance: £3,609.96

- Net annual pay: £56,958.08

- Net monthly pay: £4,746.51

- Net weekly pay: ~£1,095

£80,000 salary after tax in the UK: monthly and annual breakdown

| Item | Annual | Monthly |

|---|---|---|

| Gross salary | £80,000.00 | £6,666.67 |

| 20% Income Tax | £7,539.96 | £628.33 |

| 40% Income Tax | £11,892.00 | £991.00 |

| Employee National Insurance | £3,609.96 | £300.83 |

| Take-home pay | £56,958.08 | £4,746.51 |

So for most employees in England, Wales and Northern Ireland, £80k after tax is about £4.7k per month.

£80,000 weekly take-home pay UK

If you earn £80,000 per year, your weekly take-home pay is approximately £1,095 after tax and National Insurance.

This is useful for:

- Weekly budgeting and cash flow planning

- Comparing salaried and contract income

- Understanding how much spending power you really keep

How the tax is worked out

For the 2026 to 2027 tax year, the standard Personal Allowance is £12,570. The basic rate of Income Tax is 20% up to £50,270, and income above that threshold is generally taxed at 40% for most UK taxpayers outside Scotland. Employee National Insurance is generally charged at 8% and then 2% above the upper earnings limit.

On a £80,000 salary:

- The first £12,570 is tax-free

- A portion is taxed at 20% = £7,539.96

- A larger portion is taxed at 40% = £11,892.00

- Employee National Insurance totals about £3,609.96

At £80,000, a substantial part of your income now sits in the 40% tax band. That does not mean all of your salary is taxed at 40%, but it does mean extra earnings are taxed much more heavily than at lower salary levels.

What is £80k per month before and after tax?

Before deductions, a £80,000 salary is £6,666.67 per month.

After Income Tax and National Insurance, that falls to around £4,746.51 per month.

- Gross monthly pay: £6,666.67

- Total monthly tax and NI: £1,920.16

- Net monthly pay: £4,746.51

How to manage the 40% tax band on £80,000

Once you reach £80,000, higher-rate tax is no longer a small detail on your payslip. It becomes one of the biggest reasons your net pay rises much more slowly than your gross salary.

That is why this salary level is often a sensible point to think more carefully about tax efficiency. The aim is not to avoid tax, but to make sure pay rises, bonuses and extra earnings are being handled in the most efficient way available to you.

Common strategies people consider at this level include:

- Increasing workplace pension contributions

- Using salary sacrifice where available

- Reviewing how bonuses are paid and when they are received

- Looking at the combined effect of tax, National Insurance and student loan deductions

- Focusing on long-term tax-efficient savings rather than only short-term take-home pay

For many employees, pension contributions are one of the simplest ways to improve tax efficiency. Extra pension payments can reduce the amount of income exposed to higher-rate tax while also building retirement savings.

If your employer offers salary sacrifice, that can sometimes be even more effective than a standard pension contribution because it may reduce both taxable pay and National Insurance. This can make a noticeable difference over time, especially on bonuses or larger contribution increases.

It is also worth checking whether a pay rise or bonus feels as valuable in net terms as it does in gross terms. Once 40% tax, National Insurance and possibly student loan deductions are taken into account, the actual amount you keep can be much lower than expected.

Can a SIPP help if you earn £80,000?

Yes, a SIPP (Self-Invested Personal Pension) can be a useful option if you earn £80,000 and want more control over how you manage higher-rate tax and long-term investing.

A SIPP allows you to make extra pension contributions outside your workplace scheme, often with a wider choice of funds and investments. For some people, it is a flexible way to top up pension savings after a pay rise or bonus.

At this salary, a SIPP may help you:

- Reduce the amount of income exposed to higher-rate tax

- Claim additional higher-rate pension tax relief where eligible

- Build retirement savings in a more flexible pension wrapper

- Separate additional investing from your employer pension scheme

Many SIPPs operate using relief at source, where basic-rate tax relief is added automatically. If you are a higher-rate taxpayer, you may need to claim the extra relief separately through HMRC.

A SIPP is not always better than salary sacrifice, because salary sacrifice can sometimes improve both Income Tax and National Insurance efficiency. But a SIPP can still be a strong option when you want flexibility, wider investment choice, or extra contributions outside work.

If you want to model how pension contributions could affect your monthly net pay, use our take home pay calculator.

£80k salary after tax with student loan deductions

If you still repay a student loan, your real monthly take-home will be lower. The Income Tax and National Insurance figures do not change here, but student loan deductions reduce what actually lands in your bank account.

| Scenario | Annual take-home | Monthly take-home |

|---|---|---|

| No student loan | £56,958.08 | £4,746.51 |

| Plan 1 | £52,179.08 | £4,348.26 |

| Plan 2 | £52,402.76 | £4,366.90 |

| Plan 5 | £52,008.08 | £4,334.01 |

| Postgraduate Loan only | £53,418.08 | £4,451.51 |

The matching student loan deductions are:

- Plan 1: £4,779.00 per year or £398.25 per month

- Plan 2: £4,555.32 per year or £379.61 per month

- Plan 5: £4,950.00 per year or £412.50 per month

- Postgraduate Loan only: £3,540.00 per year or £295.00 per month

At this salary, a Plan 2 borrower loses roughly £379.61 per month, while a Plan 5 borrower loses about £412.50 per month.

You can estimate your repayments using our student loan calculator.

£80,000 vs £70,000 salary UK

Moving from £70,000 to £80,000 increases your gross pay, but much of the extra income is taxed at 40%. That means the jump in take-home pay is smaller than many people expect.

You can compare salary levels using our salary comparison calculator.

Monthly budgeting on a £80,000 salary

With a take-home of around £4,334 to £4,747 per month depending on deductions, many people can usually cover:

- Mortgage or rent payments

- Bills and utilities

- Transport and commuting

- Regular savings, investing and pension top-ups

- Discretionary spending and lifestyle costs

Even so, your actual financial comfort depends heavily on housing costs, childcare, debt repayments and where you live. A salary of £80k can feel strong in many parts of the UK, but fixed costs can still take a large share of your monthly income.

What can reduce your £80k take-home pay further?

Your actual payslip may be lower if you have:

- Workplace pension contributions

- Salary sacrifice arrangements

- Student loan deductions

- Bonus payments taxed through PAYE

- Scottish Income Tax rates

To model your exact situation, use our take home pay calculator.

Is £80,000 a good salary in the UK?

In many parts of the UK, £80k is considered a strong salary and well above average full-time earnings.

- Usually strong income in most regions

- Can support saving, investing and pension contributions

- Still affected heavily by higher-rate tax and student loan deductions

What matters most is not just the headline salary, but how much of it you actually keep after tax and how efficiently you manage the portion that falls into the higher-rate band.

What should you do next?

If you are earning £80,000, you may want to:

- Review whether pension contributions could improve tax efficiency

- Estimate the impact of student loan deductions on your monthly cash flow

- Compare your pay with nearby levels such as £70k or £90k

Useful tools:

Summary

A £80,000 salary after tax in the UK works out to about £56,958.08 per year or £4,746.51 per month in 2026 using the figures provided here.

Your real take-home may be closer to £4,334 to £4,452 per month if student loan deductions apply. At this level, planning around higher-rate tax, pension contributions, salary sacrifice and SIPPs can make a meaningful difference to your long-term finances.