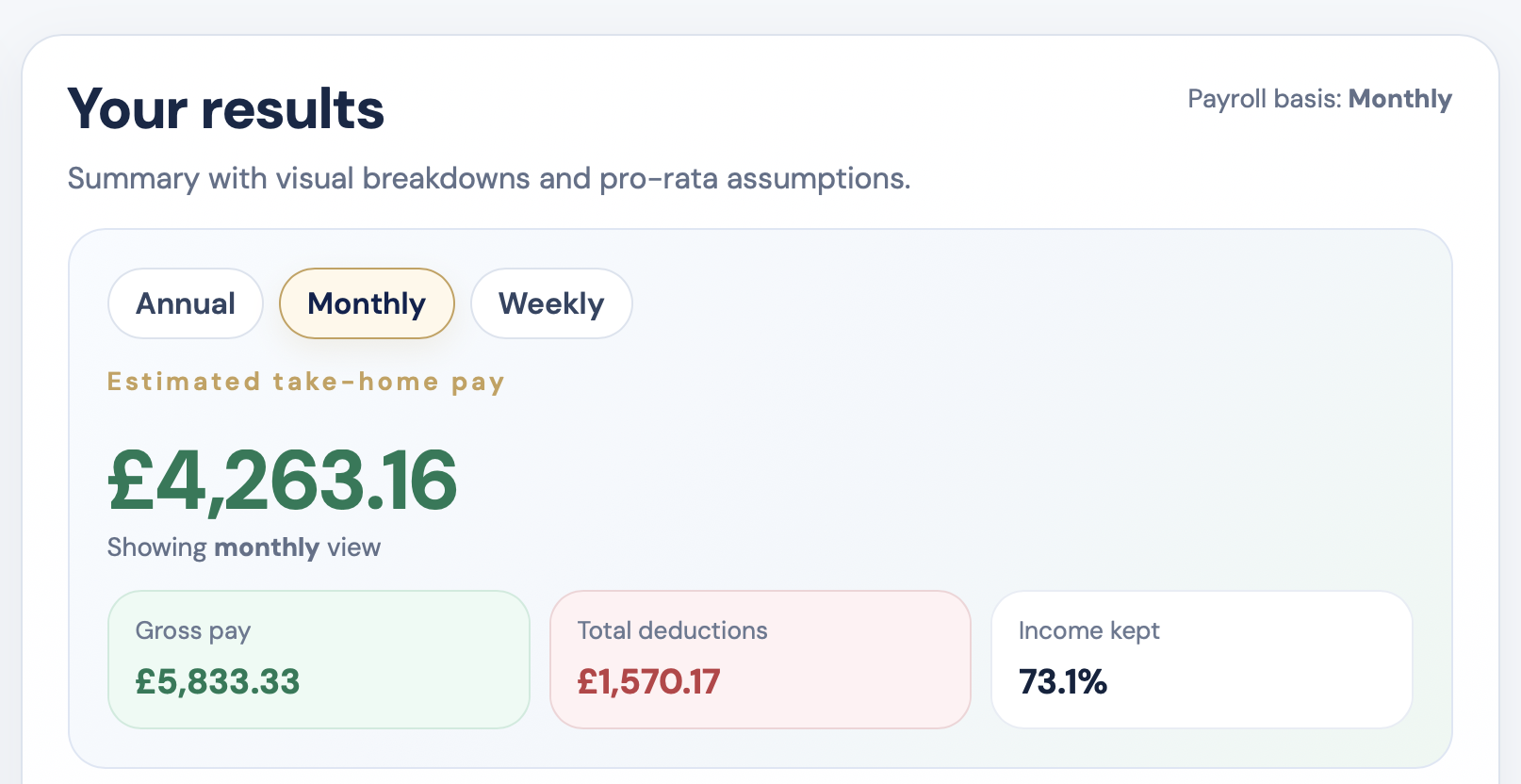

If you earn £70,000 a year, your monthly take-home pay in the UK in 2026 is roughly £4,263.16 after Income Tax and employee National Insurance, assuming you are on a standard tax code, have no pension salary sacrifice, and do not live in Scotland.

This means:

- Annual take-home pay: £51,157.96

- Monthly take-home pay: £4,263.16

- Weekly take-home pay: ~£984

This guide explains exactly how your £70,000 salary is taxed, how much you take home each month, and what factors can change your net pay.

This calculation is based on the 2026/27 UK tax year using standard HMRC rates.

If you want to test your own payslip with pension, bonus or student loan deductions, use our take home pay calculator for a personalised result.

£70,000 take-home pay UK (2026 summary)

- Gross salary: £70,000

- 20% Income Tax: £7,539.96

- 40% Income Tax: £7,892.04

- National Insurance: £3,410.04

- Net annual pay: £51,157.96

- Net monthly pay: £4,263.16

- Net weekly pay: ~£984

£70,000 salary after tax in the UK: monthly and annual breakdown

| Item | Annual | Monthly |

|---|---|---|

| Gross salary | £70,000.00 | £5,833.33 |

| 20% Income Tax | £7,539.96 | £628.33 |

| 40% Income Tax | £7,892.04 | £657.67 |

| Employee National Insurance | £3,410.04 | £284.17 |

| Take-home pay | £51,157.96 | £4,263.16 |

So for most employees in England, Wales and Northern Ireland, £70k after tax is about £4.3k per month.

£70,000 weekly take-home pay UK

If you earn £70,000 per year, your weekly take-home pay is approximately £984 after tax and National Insurance.

This is useful for:

- Weekly budgeting and spending tracking

- Comparing higher-paid roles or contract rates

- Understanding real disposable income

How the tax is worked out

For the 2026 to 2027 tax year, the standard Personal Allowance is £12,570. The basic rate of Income Tax is 20% up to £50,270, and income above that threshold is generally taxed at 40% for most UK taxpayers outside Scotland. Employee National Insurance is generally charged at 8% and then 2% above the upper earnings limit.

On a £70,000 salary:

- The first £12,570 is tax-free

- A portion is taxed at 20% = £7,539.96

- A larger portion is taxed at 40% = £7,892.04

- Employee National Insurance totals about £3,410.04

At £70,000, a significant portion of your income is now in the 40% tax band, which means marginal tax on additional earnings is much higher than at lower salary levels.

What is £70k per month before and after tax?

Before deductions, a £70,000 salary is £5,833.33 per month.

After Income Tax and National Insurance, that falls to around £4,263.16 per month.

- Gross monthly pay: £5,833.33

- Total monthly tax and NI: £1,570.17

- Net monthly pay: £4,263.16

How to manage the 40% tax band on £70,000

At £70,000, a large portion of your salary is taxed at 40%, which means careful planning can make a noticeable difference to your take-home pay and long-term wealth.

Common strategies people consider at this level include:

- Increasing workplace pension contributions

- Using salary sacrifice where available

- Managing bonus timing and structure

- Reviewing total deductions including student loans

- Focusing on tax-efficient long-term savings

One of the most effective approaches is increasing pension contributions. This can reduce the portion of income exposed to higher-rate tax while building retirement savings.

Can a SIPP help if you earn £70,000?

Yes, a SIPP (Self-Invested Personal Pension) can be a useful option at this salary level.

A SIPP allows you to make additional pension contributions outside your workplace scheme, often with more flexibility over how your money is invested.

At £70,000, you may benefit from:

- Reducing higher-rate taxable income through contributions

- Claiming additional higher-rate tax relief where eligible

- Building long-term investments in a tax-efficient environment

Many SIPPs operate using relief at source, where basic-rate tax relief is added automatically. Higher-rate taxpayers may need to claim the extra relief separately through HMRC.

If you want to model how pension contributions affect your take-home pay, use our take home pay calculator.

£70k salary after tax with student loan deductions

If you still repay a student loan, your real monthly take-home will be lower.

| Scenario | Annual take-home | Monthly take-home |

|---|---|---|

| No student loan | £51,157.96 | £4,263.16 |

| Plan 1 | £47,278.96 | £3,939.91 |

| Plan 2 | £47,502.64 | £3,958.55 |

| Plan 5 | £47,107.96 | £3,925.66 |

| Postgraduate Loan only | £48,217.96 | £4,018.16 |

The matching student loan deductions are:

- Plan 1: £3,879.00 per year or £323.25 per month

- Plan 2: £3,655.32 per year or £304.61 per month

- Plan 5: £4,050.00 per year or £337.50 per month

- Postgraduate Loan only: £2,940.00 per year or £245.00 per month

At this salary, a Plan 2 borrower loses roughly £304.61 per month, while a Plan 5 borrower loses about £337.50 per month.

You can estimate your repayments using our student loan calculator.

£70,000 vs £60,000 salary UK

Moving from £60,000 to £70,000 increases your income, but much of the additional pay is taxed at 40%, reducing the effective benefit of the increase.

You can compare salary levels using our salary comparison calculator.

Monthly budgeting on a £70,000 salary

With a take-home of around £3,900 to £4,260 per month, many people can comfortably cover:

- Housing costs and mortgage payments

- Bills and utilities

- Transport and commuting

- Regular savings and investments

- Lifestyle and discretionary spending

However, your actual financial comfort still depends heavily on location, housing costs and other commitments.

Summary

A £70,000 salary after tax in the UK works out to about £51,157.96 per year or £4,263.16 per month in 2026.

Your real take-home may be closer to £3,925 to £4,018 per month if student loan deductions apply. At this level, managing higher-rate tax through pensions and planning becomes increasingly important.